The Conversation (0)

Sort by

Advancing a premier high-grade US silver portfolio

Silver47 Exploration Corp. (TSXV: AGA) (OTCQB: AAGAF) ("Silver47" or the "Company") is pleased to announce that it has been approved for graduation from Tier 2 to Tier 1 issuer status on the TSX Venture Exchange (the "TSXV") effective May 23, 2025.

The TSXV classifies issuers into different tiers based on various factors, including financial performance, stage of development, and available resources. Tier 1 is the TSXV's highest designation and is reserved for more advanced companies with significant financial resources. This upgrade signifies Silver47's continued growth and its commitment to providing long-term value for its shareholders.

As a result of this graduation to Tier 1 status, the securities of Silver47, previously subject to the escrow provisions of Tier 2 issuers, will now be governed by the release provisions of Tier 1 issuers, with the securities being released over an 18-month period. The following securities will be immediately releasable: 3,952,748 common shares, 462,500 options, and 131,250 restricted share units and/or any common shares after the exercise of such convertible securities. The remaining escrowed securities will be releasable as follows: 3,952,763 common shares, 462,500 options, and 131,2500 restricted share units will be releasable on November 14, 2025, which is 12 months from listing (and/or any common shares after the exercise of such convertible securities); and 3,952,764 common shares, 462,500 options, and 131,250 restricted share units will be releasable on May 14, 2026, which is 18 months from listing (and/or any common shares after the exercise of such convertible securities).

About Silver47 Exploration Corp.

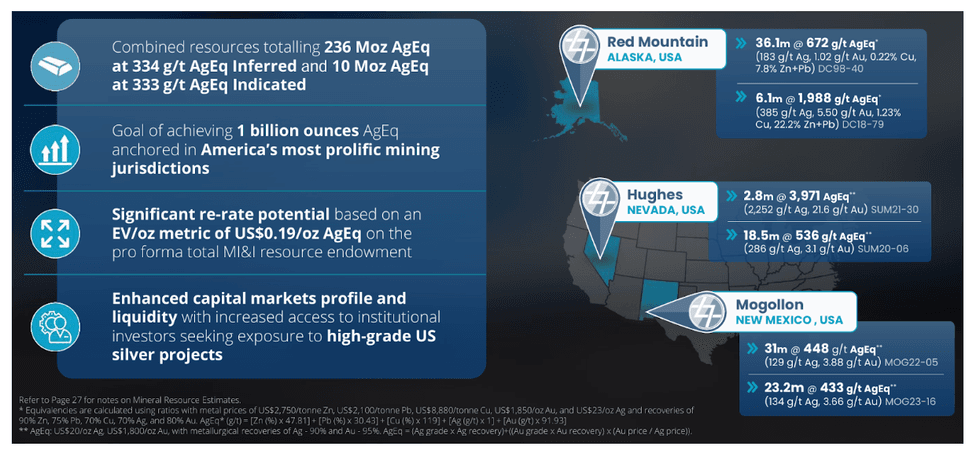

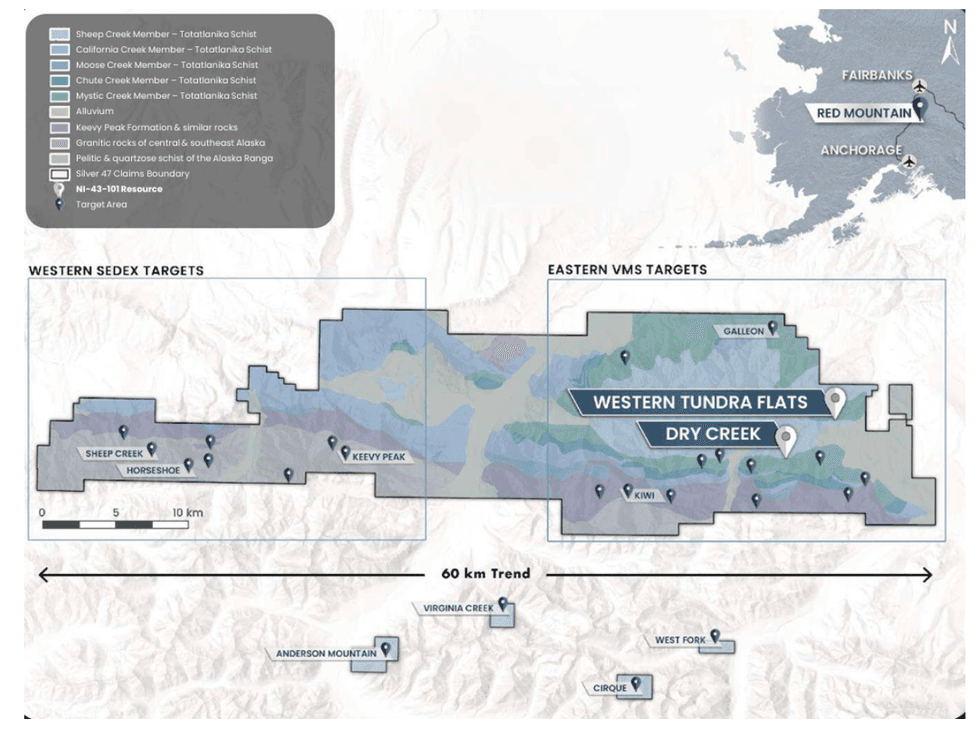

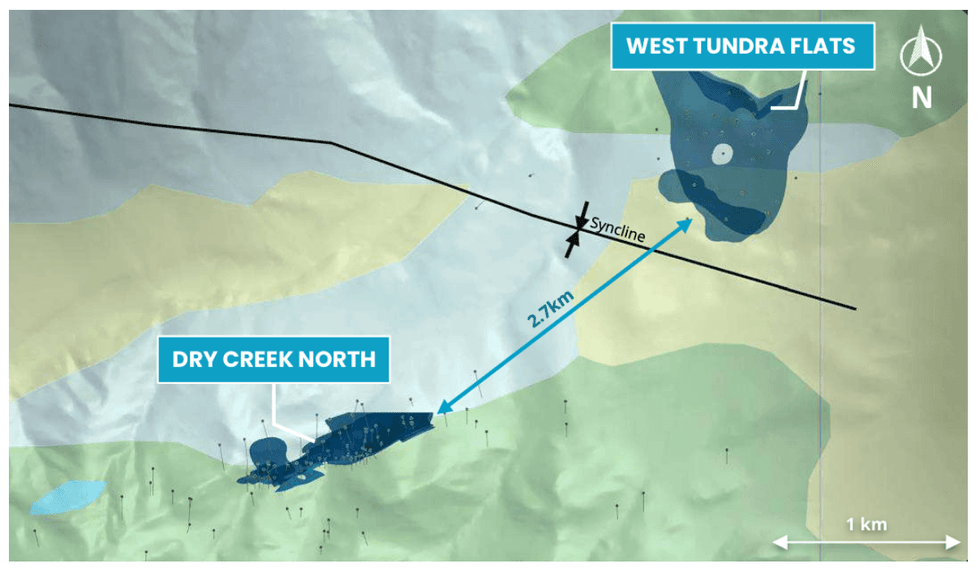

Silver47 Exploration Corp. is a Canadian-based exploration company that wholly-owns three silver and critical metals (polymetallic) exploration projects in Canada and the US. These projects include the Red Mountain Project in southcentral Alaska, a silver-gold-zinc-copper-lead-antimony-gallium VMS-SEDEX project. The Red Mountain Project hosts an inferred mineral resource estimate of 15.6 million tonnes at 7% ZnEq or 335.7 g/t AgEq, totaling 168.6 million ounces of silver equivalent, as reported in the NI 43-101 Technical Report dated March 2, 2023. The Company also owns the Adams Plateau Project in southern British Columbia, a silver-zinc-copper-gold-lead SEDEX-VMS project, and the Michelle Project in the Yukon Territory, a silver-lead-zinc-gallium-antimony MVT-SEDEX project. For detailed information regarding the resource estimates, assumptions, and technical reports, please refer to the NI 43-101 Technical Report and other filings available on SEDAR at www.sedarplus.ca. The Common Shares are traded on the TSXV under the ticker symbol AGA.

For more information about the Company, please visit www.silver47.ca and see the Technical Report filed on SEDAR+ (www.sedarplus.ca) and titled "Technical Report on the Red Mountain VMS Property Bonnifield Mining District, Alaska, USA with an effective date January 12, 2024, and prepared by APEX Geoscience Ltd.".

Follow us on social media for the latest updates:

On Behalf of the Board of Directors

Mr. Gary R. Thompson

Director and CEO

gthompson@silver47.ca

For investor relations

Meredith Eades

info@silver47.ca

778.835.2547

No securities regulatory authority has either approved or disapproved of the contents of this release. Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

FORWARD-LOOKING STATEMENTS

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "expect", "intend", "estimate", "upon" "anticipate", "believe", "continue", "plans" or similar terminology. Forward-looking statements and information include, but are not limited to: trading as a Tier 1 issuer on the TSX Venture Exchange and release from escrow of escrowed shares; the statements in regards to existing and future products of the Company; and the Company's plans and strategies. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company's actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the ability to close the Offering, including the time and sizing thereof, the insider participation in the Offering and receipt of required regulatory approvals; the use of proceeds not being as anticipated; the Company's ability to implement its business strategies; risks associated with general economic conditions; adverse industry events; stakeholder engagement; marketing and transportation costs; loss of markets; volatility of commodity prices; inability to access sufficient capital from internal and external sources, and/or inability to access sufficient capital on favourable terms; industry and government regulation; changes in legislation, income tax and regulatory matters; competition; currency and interest rate fluctuations; and the additional risks identified in the Company's financial statements and the accompanying management's discussion and analysis and other public disclosures recently filed under its issuer profile on SEDAR+ and other reports and filings with the TSXV and applicable Canadian securities regulators. The forward-looking information are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by applicable securities laws.

No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/253159

News Provided by Newsfile via QuoteMedia

Not for distribution to United States Newswire Services or for dissemination in the United States

Silver47 Exploration Corp. (TSXV: AGA) (OTCQB: AAGAF) ("Silver47" or the "Company") is pleased to announce the completion of its previously announced non-brokered private placement (the "Private Placement"), raising gross proceeds from the fourth tranche of $1,800,000 through the issuance of 3,600,000 (the "Units") at a price of $0.50 per Unit. The Company issued an aggregate of (i) 18,538,400 Units and (ii) 929,192 flow-through units of the Company (the "FT Units") at a price of $0.57 each, for aggregate gross proceeds to the Company of approximately $9.8 million under the Private Placement.

"We are extremely grateful for the strong support from our existing and new shareholders, which allowed us to upsize this private placement from $3 million to $9.8 million" Commented Gary R. Thompson, CEO "This level of support reflects the confidence in our projects and growth potential. With these funds, we are well-positioned to carry out an exciting and productive year of exploration and development at our Red Mountain Project in Alaska."

Each Unit consists of one common share in the capital of the Company (the "Common Share") and one-half of one Common Share purchase warrant (with each full warrant being a "Warrant"). Each Warrant will entitle the holder to acquire one Common Share at a price of $0.75 within 36 months following issuance.

In connection with the final closing, the Company paid aggregate finders' fees of $51,940 in cash, representing 7% of the aggregate proceeds raised by the finders, and issued 103,880 finders' warrants (the "Finders' Warrants"), representing 7% of the number of securities sold to subscribers introduced to the Company by the finders. Each Finders' Warrant is exercisable for one Common Share at an exercise price of $0.75 for a period of 36 months from the date of issuance. The Company paid aggregate finders fees of $336,234 in cash and issued 669,158 finders' warrants under the Private Placement.

All securities issued pursuant to the Private Placement are subject to a restricted hold period of four months and a day from the date of issuance under applicable Canadian securities legislation. The Private Placement remains subject to the final approval of the TSX Venture Exchange (the "TSXV").

Corporate Update

Concurrent with the completion of the Private Placement, the Company has granted to certain directors, officers, employees and consultants of the Company an aggregate of 2,600,000 stock options (the "Options"). The Options are exercisable for a 10-year period from the date of grant and will vest in two equal installments, 12 and 24 months from the date of grant. Each vested Option will entitle the holder to acquire one Common Share at an exercise of $0.60. The Options are subject to the terms and conditions of the Company's share compensation plan and the policies of the TSXV. Of the Options granted above, 300,000 Options were granted to High Tide Consulting Corp. ("High Tide"), a provider of investor relations services, pursuant to the Contractor's Agreement (as such term is defined below).

The Company has engaged the services of High Tide to provide corporate communications, investor relations and strategic marketing services in compliance with the policies of the TSXV and applicable securities laws. High Tide is expected to heighten capital market awareness and understanding of the Company and to assist with managing investor communications and expectations, through various outreach and marketing programs.

In connection with the engagement of High Tide, the Company and High Tide has entered into an independent contractor's agreement (the "Contractor's Agreement"). Pursuant to the terms of the Contractor's Agreement, the Company has agreed to pay High Tide a cash fee of C$7,500 plus applicable taxes per month and grant 300,000 Options as indicated above. The Contractor's Agreement is for an initial term of six months and may be terminated by either party on at least 30 days written notice.

High Tide is a company based in British Columbia, Canada, and offers a full suite of investor relations and communications services for public and private companies. High Tide is an arm's length party to the Company. High Tide has no present, direct or indirect interest in the Company or its securities, nor any right or present intention to acquire such an interest except as otherwise provided in this release. High Tide and its clients may acquire an interest in the securities of the Company in the future.

This news release does not constitute an offer to sell or a solicitation of an offer to buy nor shall there be any sale of any securities in any jurisdiction in which such offer, solicitation, or sale would be unlawful. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "1933 Act"), or any state securities laws and may not be offered or sold in the "United States" or to "U.S. persons" (as such terms are defined in Regulation S under the 1933 Act) unless registered under the 1933 Act and applicable state securities laws, or an exemption from such registration requirements is available.

About Silver47 Exploration Corp.

Silver47 Exploration Corp. is a Canadian-based exploration company that wholly-owns three silver and critical metals (polymetallic) exploration projects in Canada and the US. These projects include the Red Mountain Project in southcentral Alaska, a silver-gold-zinc-copper-lead-antimony-gallium VMS-SEDEX project. The Red Mountain Project hosts an inferred mineral resource estimate of 15.6 million tonnes at 7% ZnEq or 335.7 g/t AgEq, totaling 168.6 million ounces of silver equivalent, as reported in the NI 43-101 Technical Report dated March 2, 2023. The Company also owns the Adams Plateau Project in southern British Columbia, a silver-zinc-copper-gold-lead SEDEX-VMS project, and the Michelle Project in the Yukon Territory, a silver-lead-zinc-gallium-antimony MVT-SEDEX project. For detailed information regarding the resource estimates, assumptions, and technical reports, please refer to the NI 43-101 Technical Report and other filings available on SEDAR at www.sedarplus.ca. The Common Shares are traded on the TSXV under the ticker symbol AGA.

For more information about the Company, please visit www.silver47.ca and see the Technical Report filed on SEDAR+ (www.sedarplus.ca) and titled "Technical Report on the Red Mountain VMS Property Bonnifield Mining District, Alaska, USA with an effective date January 12, 2024, and prepared by APEX Geoscience Ltd.".

Follow us on social media for the latest updates:

On Behalf of the Board of Directors

Mr. Gary R. Thompson, Director and CEO

gthompson@silver47.ca

For investor relations

Meredith Eades

info@silver47.ca

778.835.2547

No securities regulatory authority has either approved or disapproved of the contents of this release. Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

FORWARD-LOOKING STATEMENTS

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "expect", "intend", "estimate", "upon" "anticipate", "believe", "continue", "plans" or similar terminology. Forward-looking statements and information include, but are not limited to: ; anticipated use of proceeds from the Private Placement; vesting and exercise of the Options; High Tide's services to be performed pursuant to the Contractor's Agreement; ability to obtain all necessary regulatory approvals; the statements in regards to existing and future products of the Company; and the Company's plans and strategies. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company's actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: ; receipt of required regulatory approvals of the Private Placement; engagement of High Tide on the terms described in the Contractors' Agreement; the use of proceeds not being as anticipated; the vesting and exercise of the Options; the Company's ability to implement its business strategies; risks associated with general economic conditions; adverse industry events; stakeholder engagement; marketing and transportation costs; loss of markets; volatility of commodity prices; inability to access sufficient capital from internal and external sources, and/or inability to access sufficient capital on favourable terms; industry and government regulation; changes in legislation, income tax and regulatory matters; competition; currency and interest rate fluctuations; and the additional risks identified in the Company's financial statements and the accompanying management's discussion and analysis and other public disclosures recently filed under its issuer profile on SEDAR+ and other reports and filings with the TSXV and applicable Canadian securities regulators. The forward-looking information are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by applicable securities laws.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/247329

News Provided by Newsfile via QuoteMedia

Silver47 Exploration Corp. (TSXV: AGA) (OTCQB: AAGAF) ("Silver47" or the "Company") is pleased to announce that, due to strong investor demand, it has increased the size of its previously announced non-brokered private placement (the "Private Placement") from $8 million to $11 million (the "Upsize"). The Company also intends to complete the third tranche (the "Third Tranche") of the Private Placement on March 21, 2025. The closing of the Third Tranche, along with the Upsize, will be completed as part of the same financing, as set out in the Company's news releases dated February 19 and 24, 2025.

Pursuant to the Third Tranche, the Company will issue approximately 3,871,000 units at a price of $0.50 each, for gross proceeds of approximately $1,935,500. Completion of the Third Tranche will result in the Company having issued an aggregate of 14,938,400 units and 929,192 flow-through units (at a price of $0.57 per flow-through unit) for aggregate proceeds under the Private Placement of $7,998,839.

Each unit under the Third Tranche will consist of one common share in the capital of the Company (the "Common Share") and one-half of one Common Share purchase warrant (with each full warrant being a "Warrant"). Each Warrant will entitle the holder to acquire one Common Share at a price of $0.75 within 36 months following issuance.

In connection with the Third Tranche, the Company will pay finders' fees of $72,975 in cash, representing 7% of the aggregate proceeds raised by such finder(s), and will issue approximately 145,950 finders' warrants (the "Finders' Warrants"), representing 7% of the number of securities sold to subscribers introduced to the Company by such finder(s). Each Finders' Warrant will be exercisable for one Common Share at an exercise price of $0.75 for a period of 36 months from the date of issuance. The Company will have paid to finders an aggregate of $284,294 in cash and issued an aggregate of 565,278 Finders' Warrants pursuant to the Private Placement to-date.

The Upsize will include the sale of the following securities:

- Up to 6,000,000 units of the Company at $0.50 each (the "Units"), for aggregate gross proceeds of up to $3 million. Each Unit will consist of one Common Share and one-half of one Warrant. Each Warrant shall entitle the holder thereof to acquire one Common Share at a price of $0.75 within 36 months following issuance.

- The Upsize is expected to close on or about April 2, 2025, or on any other date or dates as the Company may determine.

The net proceeds from the sale of the Units and the units under the Third Tranche will be used to fund exploration activities at the Red Mountain Project in Alaska and for general working capital and gross proceeds from the sale of flow-through units indicated above will be used for exploration expenditures at the Company's Adams Plateau Project in British Columbia.

Closing of the Upsize is subject to receipt of conditional acceptance from the TSX Venture Exchange ("TSXV"). All securities issuable under the Private Placement including the Upsize are subject to a hold period of four months and one day from the date of issuance under applicable securities laws.

This news release does not constitute an offer to sell or a solicitation of an offer to buy nor shall there be any sale of any securities in any jurisdiction in which such offer, solicitation, or sale would be unlawful. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "1933 Act"), or any state securities laws and may not be offered or sold in the "United States" or to "U.S. persons" (as such terms are defined in Regulation S under the 1933 Act) unless registered under the 1933 Act and applicable state securities laws, or an exemption from such registration requirements is available.

About Silver47 Exploration Corp.

Silver47 Exploration Corp. is a Canadian-based exploration company that wholly-owns three silver and critical metals (polymetallic) exploration projects in Canada and the US. These projects include the Red Mountain Project in southcentral Alaska, a silver-gold-zinc-copper-lead-antimony-gallium VMS-SEDEX project. The Red Mountain Project hosts an inferred mineral resource estimate of 15.6 million tonnes at 7% ZnEq or 335.7 g/t AgEq, totaling 168.6 million ounces of silver equivalent, as reported in the NI 43-101 Technical Report dated March 2, 2023. The Company also owns the Adams Plateau Project in southern British Columbia, a silver-zinc-copper-gold-lead SEDEX-VMS project, and the Michelle Project in the Yukon Territory, a silver-lead-zinc-gallium-antimony MVT-SEDEX project. For detailed information regarding the resource estimates, assumptions, and technical reports, please refer to the NI 43-101 Technical Report and other filings available on SEDAR at www.sedarplus.ca. Silver47's shares are traded on the TSXV under the ticker symbol AGA.

For more information about the Company, please visit www.silver47.ca and see the Technical Report filed on SEDAR+ (www.sedarplus.ca) and titled "Technical Report on the Red Mountain VMS Property Bonnifield Mining District, Alaska, USA with an effective date January 12, 2024, and prepared by APEX Geoscience Ltd."

Follow us on social media for the latest updates:

On Behalf of the Board of Directors

Mr. Gary R. Thompson, Director and CEO

gthompson@silver47.ca

For investor relations

Meredith Eades

info@silver47.ca

778.835.2547

No securities regulatory authority has either approved or disapproved of the contents of this release. Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

FORWARD-LOOKING STATEMENTS

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "expect", "intend", "estimate", "upon" "anticipate", "believe", "continue", "plans" or similar terminology. Forward-looking statements and information include, but are not limited to: closing of the Third Tranche and the Additional Offering, including the number of securities issued in respect thereof; anticipated use of proceeds; expected closing date of the Third Tranche and the Additional Offering; payment of finder's fees; ability to obtain all necessary regulatory approvals; the statements in regards to existing and future products of the Company; and the Company's plans and strategies. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company's actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the ability to close the Third Tranche and the Additional Offering, including the time and sizing thereof, and receipt of required regulatory approvals; the use of proceeds not being as anticipated; the Company's ability to implement its business strategies; risks associated with general economic conditions; adverse industry events; stakeholder engagement; marketing and transportation costs; loss of markets; volatility of commodity prices; inability to access sufficient capital from internal and external sources, and/or inability to access sufficient capital on favourable terms; industry and government regulation; changes in legislation, income tax and regulatory matters; competition; currency and interest rate fluctuations; and the additional risks identified in the Company's financial statements and the accompanying management's discussion and analysis and other public disclosures recently filed under its issuer profile on SEDAR+ and other reports and filings with the TSXV and applicable Canadian securities regulators. The forward-looking information are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by applicable securities laws.

Not for distribution to United States Newswire Services or for dissemination in the United States

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/245296

News Provided by Newsfile via QuoteMedia

Silver47 Exploration Corp. (TSXV: AGA) ("Silver47" or the "Company") is pleased to announce the closing of an additional tranche (the "Additional Tranche") of its previously announced non-brokered private placement (the "Private Placement") (as set out in the Company's news releases dated February 19 and 24, 2025). Pursuant to the closing of the Additional Tranche, the Company issued 4,155,000 units of the Company (the "Units") at a price of $0.50 each for aggregate gross proceeds to the Company of $2,077,500. The Company anticipates completing the balance of the Private Placement on or around March 19, 2025 or as may be determined by the Company.

Each Unit consists of one common share in the capital of the Company (a "Common Share") and one-half of one Common Share purchase warrant (a "Half-Warrant", with two Half-Warrants being referred to as a "Warrant"). Each Warrant entitles the holder thereof to acquire one Common Share at a price of $0.75 within 36 months following issuance. The Company intends to use the net proceeds from the sale of the Units to fund exploration activities at the Red Mountain Project in Alaska and for general working capital.

In connection with the Additional Tranche, the Company paid certain persons ("Finders") finders' fees totaling $10,220 in cash, representing 7% of the aggregate proceeds raised by the Finders, and issued 20,440 finders' warrants (the "Finder's Warrants"), representing 7% of the number of securities sold to subscribers introduced to the Company by the Finders. Each Finder's Warrant is exercisable for one Common Share at an exercise price of $0.75 for a period of 36 months from the date of issuance.

All securities issued under the Private Placement are subject to a hold period of four months and one day from the date of issuance under applicable securities laws. The Private Placement is subject to the final approval of the TSX Venture Exchange (the "TSXV") to be obtained on completion of the Private Placement.

This news release does not constitute an offer to sell or a solicitation of an offer to buy nor shall there be any sale of any securities in any jurisdiction in which such offer, solicitation, or sale would be unlawful. The securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the "1933 Act"), or any state securities laws and may not be offered or sold in the "United States" or to "U.S. persons" (as such terms are defined in Regulation S under the 1933 Act) unless registered under the 1933 Act and applicable state securities laws, or an exemption from such registration requirements is available.

About Silver47 Exploration Corp.

Silver47 wholly-owns three silver and critical metals (polymetallic) exploration projects in Canada and the US: the Flagship Red Mountain silver-gold-zinc-copper-lead-antimony-gallium VMS-SEDEX project in southcentral Alaska; the Adams Plateau silver-zinc-copper-gold-lead SEDEX-VMS project in southern British Columbia, and the Michelle silver-lead-zinc-gallium-antimony MVT-SEDEX Project in Yukon Territory. Silver47 Exploration Corp. shares trade on the TSXV under the ticker symbol AGA. For more information about Silver47, please visit our website at www.silver47.ca.

On Behalf of the Board of Directors

Mr. Gary R. Thompson

Director and CEO

gthompson@silver47.ca

For investor relations

Meredith Eades

info@silver47.ca

778.835.2547

No securities regulatory authority has either approved or disapproved of the contents of this release. Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

FORWARD-LOOKING STATEMENTS

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "expect", "intend", "estimate", "upon" "anticipate", "believe", "continue", "plans" or similar terminology. Forward-looking statements and information include, but are not limited to: closing of the Private Placement, including the number of Units and FT Units issued in respect thereof; anticipated use of proceeds; expected closing date of the Private Placement; payment of finder's fees; ability to obtain all necessary regulatory approvals; insider participation in the Private Placement; the statements in regards to existing and future products of the Company; and the Company's plans and strategies. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company's actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the ability to close the Private Placement, including the time and sizing thereof, the insider participation in the Private Placement and receipt of required regulatory approvals; the use of proceeds not being as anticipated; the Company's ability to implement its business strategies; risks associated with general economic conditions; adverse industry events; stakeholder engagement; marketing and transportation costs; loss of markets; volatility of commodity prices; inability to access sufficient capital from internal and external sources, and/or inability to access sufficient capital on favourable terms; industry and government regulation; changes in legislation, income tax and regulatory matters; competition; currency and interest rate fluctuations; and the additional risks identified in the Company's financial statements and the accompanying management's discussion and analysis and other public disclosures recently filed under its issuer profile on SEDAR+ and other reports and filings with the TSXV and applicable Canadian securities regulators. The forward-looking information are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by applicable securities laws.

No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements.

NOT FOR DISTRIBUTION TO U.S. NEWSWIRE SERVICES OR FOR DISTRIBUTION OR DISSEMINATION IN OR INTO THE U.S.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/244400

News Provided by Newsfile via QuoteMedia

Silver47 Exploration Corp. (TSXV: AGA) ("Silver47" or the "Company") is pleased to announce that, effective March 10, 2025, its shares will commence trading on the OTCQB Venture Market under the ticker symbol AAGAF. This milestone marks a key step in the Company's growth strategy and enhances its visibility to U.S. investors.

The quotation on the OTCQB® is a significant development for Silver47, as it broadens the Company's investor base and increases access to the U.S. market. With a focus on precious and base metals exploration, at its flagship Red Mountain Project in Alaska, the quotation will facilitate Silver47's continued growth and further support its upcoming exploration and development activities.

Gary R. Thompson, CEO of Silver47, commented, "Trading on the OTCQB® offers greater access for U.S.-based investors, making it easier for them to participate in the growth of Silver47. This listing is an important milestone as we strengthen our presence in the U.S. market, attract new capital, and continue advancing our project in Alaska."

The quotation on the OTCQB will provide U.S. investors with easier access to the Company's shares, real-time trading information, and up-to-date financial disclosures. This move aligns with Silver47's long-term strategy to expand its market presence and attract investment capital from the U.S. to support its exploration initiatives.

About Silver47 Exploration Corp.

Silver47 wholly-owns three silver and critical metals (polymetallic) exploration projects in Canada and the US: the Flagship Red Mountain silver-gold-zinc-copper-lead-antimony-gallium VMS-SEDEX project in southcentral Alaska; the Adams Plateau silver-zinc-copper-gold-lead SEDEX-VMS project in southern British Columbia, and the Michelle silver-lead-zinc-gallium-antimony MVT-SEDEX Project in Yukon Territory. Silver47 Exploration Corp. shares trade on the TSX-V under the ticker symbol AGA. For more information about Silver47, please visit our website at www.silver47.ca.

Follow us on social media for the latest updates:

On Behalf of the Board of Directors

Mr. Gary R. Thompson

Director and CEO

gthompson@silver47.ca

For investor relations

Meredith Eades

info@silver47.ca

778.835.2547

No securities regulatory authority has either approved or disapproved of the contents of this release. Neither the TSXV nor its Regulation Services Provider (as that term is defined in the policies of the TSXV) accepts responsibility for the adequacy or accuracy of this release.

FORWARD-LOOKING STATEMENTS

This release contains certain "forward looking statements" and certain "forward-looking information" as defined under applicable Canadian securities laws. Forward-looking statements and information can generally be identified by the use of forward-looking terminology such as "may", "will", "expect", "intend", "estimate", "upon" "anticipate", "believe", "continue", "plans" or similar terminology. Forward-looking statements and information include, but are not limited to: expected benefits from the OTC quotation and first trading date. Forward-looking statements and information are based on forecasts of future results, estimates of amounts not yet determinable and assumptions that, while believed by management to be reasonable, are inherently subject to significant business, economic and competitive uncertainties and contingencies. Forward-looking statements and information are subject to various known and unknown risks and uncertainties, many of which are beyond the ability of the Company to control or predict, that may cause the Company's actual results, performance or achievements to be materially different from those expressed or implied thereby, and are developed based on assumptions about such risks, uncertainties and other factors set out herein, including but not limited to: the ability to close the Offering, including the time and sizing thereof, the insider participation in the Offering and receipt of required regulatory approvals; the use of proceeds not being as anticipated; the Company's ability to implement its business strategies; risks associated with general economic conditions; adverse industry events; stakeholder engagement; marketing and transportation costs; loss of markets; volatility of commodity prices; inability to access sufficient capital from internal and external sources, and/or inability to access sufficient capital on favourable terms; industry and government regulation; changes in legislation, income tax and regulatory matters; competition; currency and interest rate fluctuations; and the additional risks identified in the Company's financial statements and the accompanying management's discussion and analysis and other public disclosures recently filed under its issuer profile on SEDAR+ and other reports and filings with the TSXV and applicable Canadian securities regulators. The forward-looking information are made based on management's beliefs, estimates and opinions on the date that statements are made and the Company undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances should change, except as required by applicable securities laws.

No forward-looking statement can be guaranteed, and actual future results may vary materially. Accordingly, readers are advised not to place undue reliance on forward-looking statements.

To view the source version of this press release, please visit https://www.newsfilecorp.com/release/243882

News Provided by Newsfile via QuoteMedia

HIGHLIGHTS

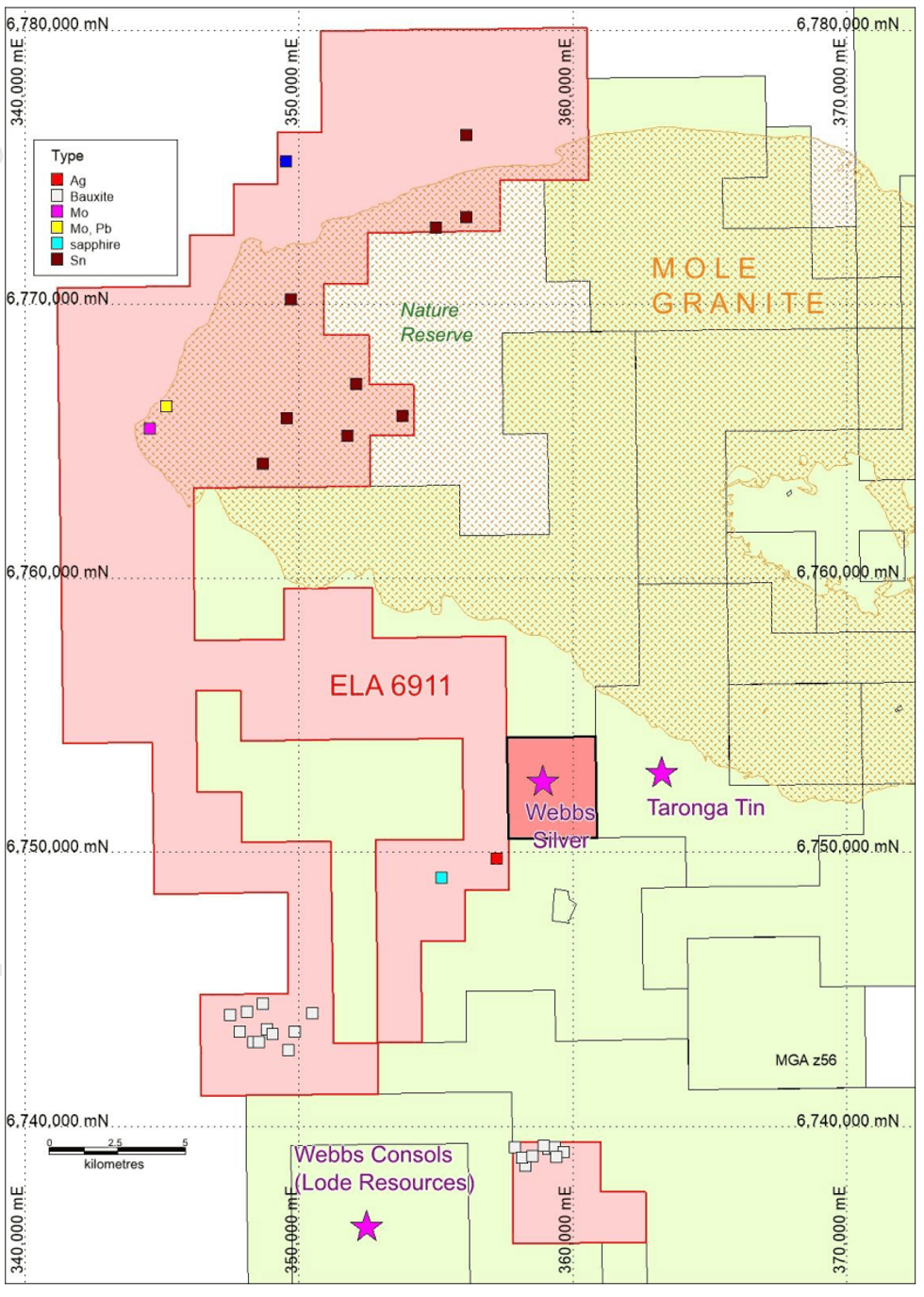

Figure 1: New ELA 6911 showing proximity to the Webbs Silver, Webbs Consols, and Taronga Tin deposits: Mole River Granite shown as orange stipple.

Figure 1: New ELA 6911 showing proximity to the Webbs Silver, Webbs Consols, and Taronga Tin deposits: Mole River Granite shown as orange stipple.

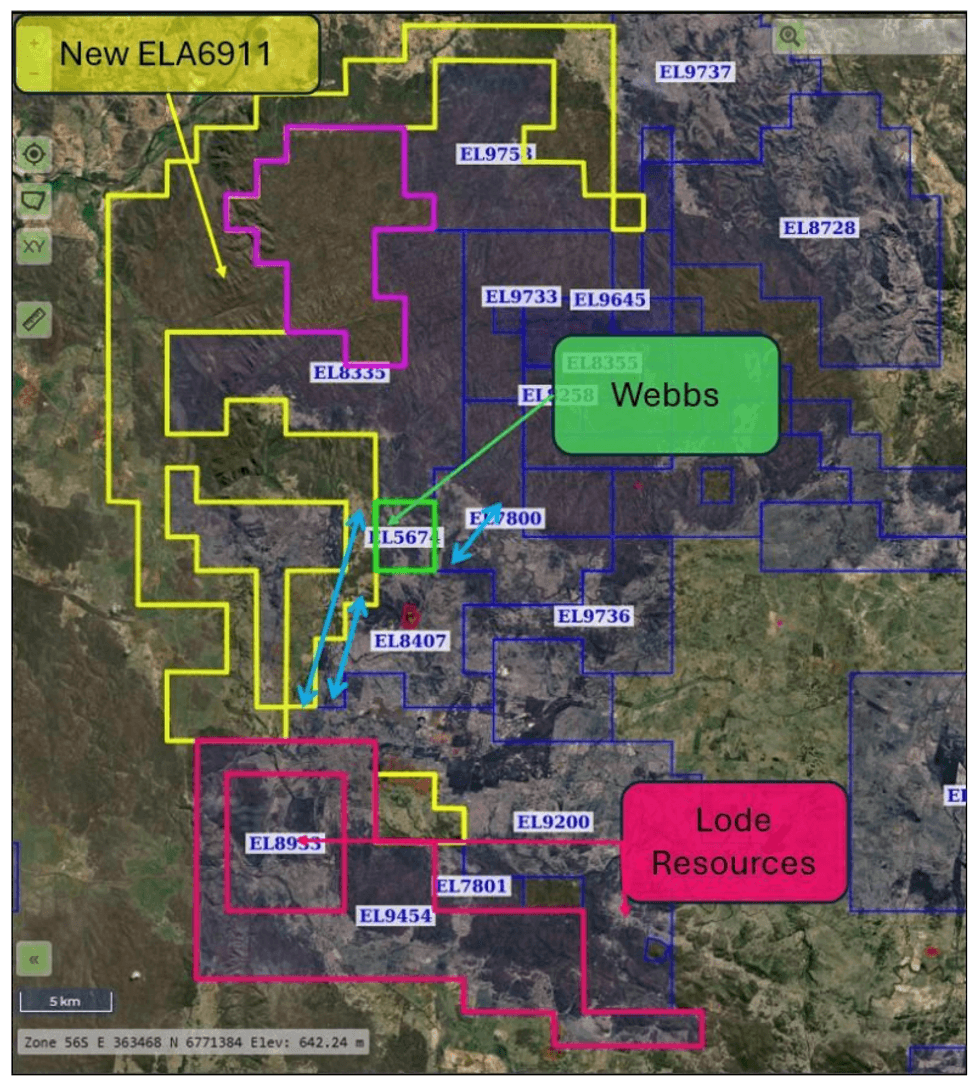

Figure 2: New ELA 6911 in yellow showing Webbs Silver in green; competitor tenements; and potential silver trends in light blue.

Figure 2: New ELA 6911 in yellow showing Webbs Silver in green; competitor tenements; and potential silver trends in light blue.

Commenting on the acquisition of this large new land holding, Rapid Critical Metals’ Managing Director, Martin Holland, said:

“It’s exciting to see the new proposed managing director, Byron Miles, adding value to Rapid even before the transaction has completed. This new land holding fits perfectly with our priorities of expanding the JORC resources of Webbs and finding new discoveries in the district”.

Click here for the full ASX Release

This article includes content from Rapid Critical Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

Thank you for requesting our exclusive Investor Report!

This forward-thinking document will arm you with the insights needed to make well-informed decisions for 2025 and beyond.

"I'm looking for US$40 (per ounce) or so in 2025. It's really hard to predict because technically there's no resistance above US$35 or so”

— David Morgan, the Morgan Report

The Investing News Network is a growing network of authoritative publications delivering independent, unbiased news and education for investors. We deliver knowledgeable, carefully curated coverage of a variety of markets including gold, cannabis, biotech and many others. This means you read nothing but the best from the entire world of investing advice, and never have to waste your valuable time doing hours, days or weeks of research yourself.

At the same time, not a single word of the content we choose for you is paid for by any company or investment advisor: We choose our content based solely on its informational and educational value to you, the investor.

So if you are looking for a way to diversify your portfolio amidst political and financial instability, this is the place to start. Right now.

Silver Price Forecast: Top Trends for Silver in 2025

The silver price reached highs not seen since 2012 this past year, supported by an ongoing deficit and increasing interest from investors as geopolitical concerns prompted safe-haven buying.

The white metal reached its highest point for the year in October, breaking through US$34 per ounce on the back of a shifting post-pandemic landscape and geopolitical tensions. However, Donald Trump's victory in the US presidential election just a few weeks later buoyed bond yields and the US dollar while weighing on silver and gold.

What will 2025 hold for silver? As the new year approaches, investors are closely watching how Trump's policies and actions could impact the precious metal, along with supply and demand trends in the space.

Here's what experts see coming for silver in 2025.

As Trump's inauguration approaches, speculation is rife about how he could affect the resource industry.

The president-elect ran on a policy of “drill, baby, drill," and while his focus was largely on oil and gas companies, mining sector participants have taken it as a positive sign for exploration and development.

Trump's promise to reduce permitting timelines for anyone making an investment of US$1 billion or more in the US has excited sector members, and could end up being a boon to silver companies in the country.

However, part of the help Trump has promised to mining companies comes from reneging on environmental commitments, including the Paris Agreement. This could end up weighing on silver.

Current President Joe Biden's Inflation Reduction Act includes tax credits and deductions for solar projects, and there's some concern that the incoming administration and the new Elon Musk-led Department of Government Efficiency (DOGE) could impose reversals or have the entire act gutted, hurting the solar market.

However, Peter Krauth, author of "The Great Silver Bull" and editor of the Silver Stock Investor, told the Investing News Network (INN) that Tesla (NASDAQ:TSLA) CEO Musk could end up keeping solar safe.

“Tesla bought SolarCity, which became Tesla Energy. They are an important provider of solar panels. Again, Musk’s new role heading DOGE and obvious close connection to Trump just might help mitigate risks to Tesla and its solar panel/power storage business. If that happens, in whatever form it may take, it could shelter solar panel production and sales in the US to a considerable degree,” Krauth explained via email.

He also noted that Trump's presidency isn't without risks and that much uncertainty still remains.

Mind Money CEO Julia Khandoshko also isn't worried about solar demand in the US.

“Rolling back ESG policies and returning to carbon-based technologies could slow the green energy transition in the US. However, Europe and China, the main drivers of the green transition, remain committed to clean energy, which increases silver demand. Thus, global trends will continue to support silver use in renewable energy technologies,” she told INN.

Industrial segments have been critical for silver demand in recent years.

As of November, the Silver Institute was forecasting total industrial demand of 702 million ounces of silver for 2024, an increase of 7 percent over the 655 million ounces recorded in 2023.

The institute attributes much of this increase to energy transition sectors, highlighting photovoltaics in particular.

However, these gains are coming alongside flat mine production, which is expected to grow only 1 percent to 837 million ounces during 2024. Once factored in, secondary supply from recycling pushes total supply of silver to 1.03 billion ounces for the year, a considerable gap from the 1.21 billion ounces of total demand.

Both Krauth and Khandoshko think the gap between silver supply and demand will continue.

Krauth suggested that companies have been dipping into aboveground inventories to narrow the gap, which has helped to keep the price of silver from exploding over the past year. "That supply is quickly drying up, so I expect to see renewed upward price pressure since silver miners are unable to grow output," he told INN.

Khandoshko expressed a similar sentiment, saying demand is likely to keep outpacing supply.

However, she also sees geopolitics and a global macroeconomic situation that could constrain both demand and supply growth in 2025. For example, economic difficulties in Europe and China could slow energy transition demand.

"The problem is that silver production is mainly concentrated in geopolitically challenging areas, such as Russia and Kazakhstan, where securing funding for supply expansion is quite difficult" — Julia Khandoshko, Mind Money

When it comes to supply, Khandoshko told INN that she sees a different scenario.

“The problem is that silver production is mainly concentrated in geopolitically challenging areas, such as Russia and Kazakhstan, where securing funding for supply expansion is quite difficult," she explained.

"These factors limit silver’s growth potential compared to gold, which in turn benefits from its role as a safe-haven asset during times of economic uncertainty."

As silver supply becomes increasingly stressed, experts are eyeing projects that are ramping up.

Krauth highlighted Aya Gold and Silver’s (TSX:AYA:OTCQX:AYASF) Zgounder mine expansion. Its first pour was at the end of November, and it is expected to ramp up to full annual output of 8 million ounces in 2025.

Endeavour Silver’s (TSX:EDR,NYSE:EXK) Terronera mine is also nearing completion. Once complete, the operation is expected to produce 15.5 million silver equivalent ounces per year.

For its part, Skeena Resources (TSX:SKE,NYSE:SKE) is working to develop its Eskay Creek project. It is set to come online in 2027, and is expected to bring 9.5 million ounces of silver per year to market in its first five years.

Krauth said a rising silver price is likely good news for mergers and acquisitions in 2025.

“Higher prices, since they translate into higher share prices, meaning acquirers can use their more valuable shares as a currency to acquire others … I think 2024 will bring deals between mid-tiers and between juniors," he said.

Krauth added, "The truth is that many mid-tier producers have not been spending on exploration. Something has to give, so I think we’ll see this space heat up."

Khandoshko and Krauth have similar silver outlooks for 2025, suggesting a possible pullback.

“Due to supply shortages and increasing demand in the coming months, silver is expected to reach US$35. After this, a slight pullback to US$30 would be possible,” Khandoshko said.

However, after that happens she projects another rise, with silver potentially passing US$50.

Krauth was looking for silver to reach US$35 in 2024, which happened in Q4. Looking forward to 2025, he thinks the white metal will revisit that level in the first quarter, with US$40 or more possible later in the year.

However, he suggested that investors should be cautious of wider economic trends affecting silver.

“There is a serious risk of significant correction in the broader markets and of a recession. A broad market selloff could bleed into silver stocks, even if only temporarily,” Krauth said.

In the case of a recession, a lack of industrial demand could create headwinds for silver. Still, Krauth thinks that could be tempered by government stimulus efforts for green energy and infrastructure.

Overall, 2025 could be a significant year for silver investors. However, geopolitical and economic instability may provide headwinds across the resource sector and could stymie silver's upward momentum.

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: Prismo Metals is a client of the Investing News Network. This article is not paid-for content.

The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Gold may be grabbing headlines with record-breaking highs in 2025, but silver is quietly making its own impressive climb, rising 17 percent since the start of the year.

Long supported by industrial demand, the silver market is also benefiting from its reputation as a safe-haven asset. However, mounting economic uncertainty has rattled investors in recent months.

While there are many driving forces behind this uncertainty, the ongoing tariff threats from US President Donald Trump and his administration have spooked equity markets worldwide.

After reaching a year-to-date high of US$34.72 per ounce in October 2024, the price of silver spent the rest of the year in decline, bottoming out at US$28.94 on December 30.

A momentum shift at the start of the year caused it to rise. Opening at US$29.53 on January 2, silver quickly broke through the US$30 barrier on January 7, eventually reaching US$31.28 by January 31.

Silver price, January 2 to April 4, 2025

Chart via Trading Economics.

Silver's gains continued through much of February, with the white metal climbing to US$32.94 on February 20 before retreating to US$31.13 on February 28. Silver rose again in March, surpassing the US$32 mark on March 5 and closing above US$32 on March 12. It peaked at its quarterly high of US$34.43 on March 27.

Heading into April, silver slumped back to US$33.67 on the first day of the month; it then declined sharply to below US$30 following Trump's tariff announcements on April 2.

Precious metals, including silver, have benefited from the volatility created by the Trump administration’s constant tariff threats since the beginning of the year. These threats have caused chaos throughout global equity and financial markets, prompting more investors to seek safe-haven assets to stabilize their portfolios.

However, there are concerns that the threat of tariffs could weaken industrial demand, which could cool price gains in the silver market. In an email to the Investing News Network (INN), Peter Krauth, editor of the Silver Stock Investor and author of "The Great Silver Bull," said it's too soon to tell how tariffs may affect silver.

“We don’t really have any indication yet that industrial demand has weakened. There is, of course, a lot of concern regarding industrial demand, as tariffs could cause demand destruction as costs go up,” he said.

Krauth noted that for solar panels there is an argument that tariffs could positively affect industrial demand if countries have a greater desire for self-sufficiency and reduced reliance on energy imports.

He referenced research by Heraeus Precious Metals about a possible slowdown in demand from China, which accounts for 80 percent of solar panel capacity. However, any slowdown would coincide with a transition from older PERC technology to newer TOPCon cells, which require significantly more silver inputs.

“This, along with the gradual replacement of older PERC solar panels with TOPCon panels, should support silver demand at or near recent levels,” Krauth said.

Another potential headwind for silver is the looming prospect of a recession in the US.

At the beginning of 2024, analysts had largely reached a consensus that some form of recession was inevitable.

While real GDP in the US rose 2.8 percent year-on-year for 2024, data from the Federal Reserve Bank of Atlanta’s GDPNow tool shows a projected -2.8 percent growth rate for the first quarter.

The Bureau of Economic Analysis won't release official real GDP figures until April 30, but the Atlanta Fed’s numbers suggest a troubling fall in GDP that could signal an impending recession.

In comments to INN, Mind Money CEO Julia Khandoshko indicated that a recession may negatively impact the silver market due to the growing demand for silver from energy transition markets.

“When the economy slows down, demand for manufactured goods, including silver, decreases, which means that buying in the next six months is unlikely to be a wise decision,” she said.

Solar panels account for significant demand, with considerable amounts also used in electric vehicles. Tariffs on US vehicle imports and a possible recession could create added pressure for silver.

"In my view, there’s a strong possibility of witnessing a shock from a severe supply shortage in the silver market within the next six months or so" — Peter Krauth, Silver Stock Investor

“Another important factor is silver’s connection to the electric vehicle market. Previously, this sector supported demand for the metal, but now its growth has slowed down. In Europe and China, interest in electric cars is no longer so active, and against the background of economic problems, sales may even decline,” Khandoshko said.

Silver demand from solar panel production stands at 232 million ounces annually, with an additional 80 million ounces used by the electric vehicle sector. A recession could lead consumers to postpone major purchases, such as home improvements or new vehicles, particularly if coupled with the extra costs of tariffs.

Although the impact of tariffs on the economy — and ultimately demand for silver — remains uncertain, the Silver Institute’s latest news release on March 3 indicates a fifth consecutive annual supply deficit.

“I think silver will hold up well and rise on balance over the rest of this year,” Krauth said.

He also noted that, like gold, there have been shipments of physical silver out of vaults in the UK to New York as market participants try to avoid any direct tariffs that may be coming.

“In my view, there’s a strong possibility of witnessing a shock from a severe supply shortage in the silver market within the next six months or so,” Krauth explained to INN.

Khandoshko suggested silver's outlook is more closely tied to consumer sentiment. “The situation may also change when the news stops discussing the high probability of a recession in the US,” she remarked.

With Trump announcing a sweeping 10 percent global tariff along with dozens of specific reciprocal tariffs on April 2, there appears to be more instability and uncertainty ahead for the world’s financial systems.

This uncertainty has spread to precious metals, with silver trading lower on April 3 and retreating back toward the US$31 mark. Investors might be taking profits, but it could also be a broader pullback as they determine how to respond in a more aggressively tariffed world. In either scenario, the market may be nearing opportunities.

“There is some risk that we could see a near-term correction in the silver price. I don’t see silver as currently overbought, but gold does appear to be. I think we could get a correction in the gold price, which would likely pull silver lower. I could see silver retreating to the US$29 to US$30 level. That would be an excellent entry point. In that scenario, I’d be a buyer of both the physical metal and the silver miners,” Krauth said.

With increased industrial demand and its traditional safe-haven status, silver may present a more ideological challenge for investors in 2025 as competing forces exert their influence. Ultimately, supply and demand will likely be what drives investors to pursue opportunities more than its safe-haven appeal.

Don’t forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

Editorial Disclosure: The Investing News Network does not guarantee the accuracy or thoroughness of the information reported in the interviews it conducts. The opinions expressed in these interviews do not reflect the opinions of the Investing News Network and do not constitute investment advice. All readers are encouraged to perform their own due diligence.

Silver-mining companies and juniors have seen support from a strong silver price in 2025. Since the start of the year, the price of silver has increased by over 11 percent as of April 11, and it reached a year-to-date high of US$34.38 per ounce on March 27.

Silver’s dual function as a monetary and industrial metal offers great upside. Demand from energy transition sectors, especially for use in the production of solar panels, has created tight supply and demand forces.

Demand is already outpacing mine supply, making for a positive situation for silver-producing companies.

So far, aboveground stockpiles have been keeping the price in check, but the expectation is those stocks will be depleted in 2025 or 2026, further restricting the supply side of the market.

How has silver's price movement benefited Canadian silver stocks on the TSX, TSXV and CSE? The five companies listed below have seen the best performances since the start of the year. Data was gathered using TradingView's stock screener on February 12, 2025, and all companies listed had market caps over C$10 million at that time.

Year-to-date gain: 185.92 percent

Market cap: C$848.98 million

Share price: C$2.03

Discovery Silver is a precious metals development company focused on advancing its Cordero silver project in Mexico. Additionally, it is looking to become a gold producer with its recently announced acquisition of the producing Porcupine Complex in Ontario, Canada.

Cordero is located in Mexico’s Chihuahua State and is composed of 26 titled mining concessions covering approximately 35,000 hectares in a prolific silver and gold mining district.

A 2024 feasibility study for the project outlines proven and probable reserves of 327 million metric tons of ore containing 302 million ounces of silver at an average grade of 29 grams per metric ton (g/t) silver, and 840,000 ounces of gold at an average grade of 0.08 g/t gold. The site also hosts significant zinc and lead reserves.

The report also indicated favorable economics for development. At a base case scenario of US$22 per ounce of silver and US$1,600 per ounce of gold, the project has an after-tax net present value of US$1.18 billion, an internal rate of return of 22 percent and a payback period of 5.2 years.

Discovery's shares gained significantly on January 27, after the company announced it had entered into a deal to acquire the Porcupine Complex in Canada from Newmont (TSX:NGT,NYSE:NEM).

The Porcupine Complex is made up of four mines including two that are already in production: Hoyle Pond and Borden. Additionally, a significant portion of the complex is located in the Timmins Gold Camp, a region known for historic gold production.

Discovery anticipates production of 285,000 ounces of gold annually over the next 10 years and has a mine life of 22 years. Inferred resources at the site point to significant expansion, with 12.49 million ounces of gold, from 254.5 million metric tons of ore with an average grade of 1.53 g/t.

Upon the closing of the transaction, Discovery will pay Newmont US$200 million in cash and US$75 million in common shares, and US$150 million of deferred consideration will be paid in four payments beginning on December 31, 2027.

According to Discovery in its full-year 2024 financial results, the Porcupine acquisition will help support the financing, development and operation of Cordero. Discovery’s share price reached a year-to-date high of C$2.12 on March 31.

Year-to-date gain: 136.36 percent

Market cap: C$16.47 million

Share price: C$0.13

Almaden Minerals is a precious metals exploration company working to advance the Ixtaca gold and silver deposit in Puebla, Mexico. According to the company website, the deposit was discovered by Almaden’s team in 2010 and has seen more than 200,000 meters of drilling across 500 holes.

A July 2018 resource estimate shows measured resources of 862,000 ounces of gold and 50.59 million ounces of silver from 43.38 million metric tons of ore, and indicated resources of 1.15 million ounces of gold and 58.87 million ounces of silver from 80.76 million metric tons of ore with a 0.3 g/t cutoff.

In April 2022, Mexico’s Supreme Court of Justice (SCJN) ruled that the initial licenses issued in 2002 and 2003 would be reverted back to application status after the court found there had been insufficient consultation when the licenses were originally assigned.

Ultimately, the applications were denied in February 2023, effectively halting progress on the Ixtaca project. While subsequent court cases have preserved Almaden’s mineral rights, it has yet to restore the licenses to continue work on the project.

In June 2024, Almaden announced it had confirmed up to US$9.5 million in litigation financing that will be used to fund international arbitrations proceedings against Mexico under the Comprehensive and Progressive Agreement for Trans-Pacific Partnership.

In a December update, the company announced that several milestones had been achieved, including the first session with the tribunal, at which the company was asked to submit memorial documents outlining its legal arguments by March 20, 2025. At that time, the company stated it would vigorously pursue the claim but preferred a constructive resolution with Mexico.

In its most recent update on March 21, the company indicated that it had submitted the requested documents, claiming US$1.06 billion in damages. The memorial document outlines how Mexico breached its obligations and unlawfully expropriated Almaden’s investments without compensation.

Shares in Almaden reached a year-to-date high of C$0.135 on February 24.

Year-to-date gain: 98.43 percent

Market cap: C$373.48 million

Share price: C$2.52

Avino Silver and Gold Mines is a precious metals miner with two primary silver assets: the producing Avino silver mine and the neighboring La Preciosa project in Durango, Mexico.

The Avino mine is capable of processing 2,500 metric tons of ore per day ore, and according to its FY24 report released on January 21 the mine produced 1.1 million ounces of silver, 7,477 ounces of gold and 6.2 million pounds of copper last year. Overall, the company saw broad production increases with silver rising 19 percent, gold rising 2 percent and copper increasing 17 percent year over year.

In addition to its Avino mining operation, Avino is working to advance its La Preciosa project toward the production stage. The site covers 1,134 hectares, and according to a February 2023 resource estimate, hosts a measured and indicated resource of 98.59 million ounces of silver and 189,190 ounces of gold.

In a January 15 update, Avino announced it had received all necessary permits for mining at La Preciosa and begun underground development at La Preciosa. It is now developing a 350-meter mine access and haulage decline. The company said the first phase at the site is expected to be under C$5 million and will be funded from cash reserves.

The latest update from Avino occurred on March 11, when it announced its 2024 financial results. The company reported record revenue of $24.4 million, up 95 percent compared to 2023. Avino also reduced its costs per silver ounce sold.

Additionally, Avino reported a 19 percent increase in production in 2024, producing 1.11 million ounces of silver compared to 928,643 ounces in 2023. The company’s sales also increased, up by 23 percent to 2.56 million ounces of silver compared to 2.09 million ounces the previous year.

Avino's share price marked a year-to-date high of C$2.80 on March 27.

Year-to-date gain: 90 percent

Market cap: C$160.17 million

Share price: C$1.90

Highlander Silver is an exploration and development company advancing projects in South America.

Its primary focus has been the San Luis silver-gold project, which it acquired in a May 2024 deal from SSR Mining (TSX:SSRM,NASDAQ:SSRM) for US$5 million in upfront cash consideration and up to an additional US$37.5 million if Highlander meets certain production milestones.

The 23,098 hectare property, located in the Ancash department of Peru, hosts a historic measured and indicated mineral resource of 9 million ounces of silver, with an average grade of 578.1 g/t, and 348,000 ounces of gold at an average grade of 22.4 g/t from 484,000 metric tons of ore.

In July 2024, the company said it was commencing field activities at the project; it has not provided results from the program. In its December 2024 management discussion and analysis, the company stated it was undertaking a review of prior exploration plans and targets, adding that it believes there is exceptional growth potential.

Highlander's most recent news came on March 11, when it announced it had closed an upsized bought deal private placement for gross proceeds of C$32 million. The company said it will use the funding to further exploration activities at San Luis and for general working capital.

Shares in Highlander reached a year-to-date high of C$1.96 on March 31.

Year-to-date gain: 85.45 percent

Market cap: C$192.16 million

Share price: C$0.51

Santacruz Silver is an Americas-focused silver producer with operations in Bolivia and Mexico. Its producing assets include the Bolivar, Porco and Caballo Blanco Group mines in Bolivia, along with the Zimapan mine in Mexico.

In a production report released on January 30, the company disclosed consolidated silver production of 6.72 million ounces, marking a 4 percent decrease from the 7 million ounces produced in 2023. This decline was primarily attributed to a reduction in average grades across all its mining properties.

In addition to its producing assets, Santacruz also owns the greenfield Soracaya project. This 8,325-hectare land package is located in Potosi, Bolivia. According to an August 2024 technical report, the site hosts an inferred resource of 34.5 million ounces of silver derived from 4.14 million metric tons of ore with an average grade of 260 g/t.

Shares in Santacruz reached a year-to-date high of C$0.59 on March 18.

Don’t forget to follow us @INN_Resource for real-time news updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.

The central bank has held its benchmark rate at 4.25 to 4.5 percent since November 2024.

Silver price, May 29 to June 5, 2025.

Chart via the Investing News Network.

CME Group's (NASDAQ:CME) FedWatch tool shows half of market respondents predict a 0.25 percent cut at the Fed's September meeting, while the other half is split on the Fed holding the line and a deeper 0.5 percent cut.

Silver's spike also comes after a phone call between US President Donald Trump and Russian President Vladimir Putin. Following the discussion, Trump said a near-term ceasefire between Russia and Ukraine is unlikely, noting that Putin has vowed to respond to recent attacks by Ukraine that destroyed more than 40 nuclear-capable aircraft.

On the economic data front, the US released its weekly unemployment insurance report on Thursday. It shows that the advance figure for seasonally adjusted initial claims was 247,000 for the week ended on May 31. The four week average has been pushed to 1.9 million, the highest level since November 27, 2021.

The US Bureau of Labor Statistics reported more data to suggest a slumping US economy in a Thursday report focused on Q1. In its release, the bureau said that nonfarm labor productivity decreased 1.5 percent in the first quarter of the year as output decreased 0.2 percent and hours worked increased 1.3 percent.

The labor news comes as the Trump administration ratcheted up tariffs on steel and aluminum products to 50 percent this week, raising the possibility of a deepening trade war, and putting greater pressure on the global economy.

Elsewhere, gold and equity markets weren’t faring as well on Thursday.

Gold was off by 0.5 percent in morning trading, falling to US$3,353.66 per ounce.

The metal has surged more than 25 percent this year, setting a slew of new price records, and has continued to trade in elevated territory, fueled by the same conditions as silver’s recent run.

The S&P 500 (INDEXSP: INX) was flat, recording a 0.14 percent decline to 5,961. The Nasdaq-100 (INDEXNASDAQ: NDX) was the sole gainer in morning trading, rising 0.24 percent to 21,776, and the Dow Jones Industrial Average (INDEXDJX: .DJI) was unchanged at 42,422.

Don't forget to follow us @INN_Resource for real-time updates!

Securities Disclosure: I, Dean Belder, hold no direct investment interest in any company mentioned in this article.