Evolving DEI Disclosure Practices in SEC Filings

Evolving DEI Disclosure Practices in SEC Filings

In the first four months of the Trump Administration, many companies have modified and, in some cases, ended their diversity, equity, and inclusion (“DEI”) related commitments, policies, programs and practices. The extent of these changes is illustrated by the fact that a large majority of the S&P 500 have significantly revised or removed DEI-related disclosures from their recent filings with the Securities and Exchange Commission (“SEC”).

We analyzed evolving DEI-related disclosure practices in recent SEC filings among major corporations, with a spotlight on the financial sector, [1] and found a marked shift in how companies disclose their approach to what was previously described as DEI. While the majority of large public companies in the US have removed references to “DEI” and related language from their SEC filings, most of these companies still have at least one diversity-related disclosure in their most recent annual report or proxy statement, reflecting a change in corporate disclosure and internal approaches to diversity-related policies, programs and practices that is still evolving.

In the first week of his administration, President Trump issued a series of executive orders regarding DEI-related programs in the public and private sectors. This included Executive Order 14173, titled “Ending Illegal Discrimination and Restoring Merit-Based Opportunity”, signed by President Trump on January 21, 2025. Executive Order 14173 rescinded several executive orders from previous administrations, including the Civil Rights Movement-era Executive Order 11246.[2] Additionally, Executive Order 14173 ordered the heads of all executive departments and agencies to “combat illegal private-sector DEI preferences, mandates, policies, programs, and activities.”

As part of this effort, Executive Order 14173 directed the Attorney General, in consultation with the heads of relevant federal agencies and in coordination with the Director of Office of Management and Budget, to submit a report containing (i) recommendations for ending “illegal discrimination and preferences” in the private sector, including DEI-related policies and practices; and (ii) a proposed “strategic enforcement plan” identifying:

- Key sectors of concern within each agency’s jurisdiction, and “the most egregious and discriminatory DEI practitioners” in each sector of concern;

- A plan to deter unlawful DEI, including identification of up to nine potential civil compliance investigations of publicly traded companies (or other large non-profits, associations, foundations or institutions of higher education); and

- Other strategies to encourage the private sector to end “illegal DEI discrimination and preferences”, including appropriate federal government litigation, intervention, regulatory action and sub-regulatory guidance.

Executive Order 14173 also imposed obligations on federal government contractors to affirmatively certify that their DEI- and other employment-related practices and procedures are fully compliant with existing federal anti-discrimination statutes—a challenging task due to the sparse case law on the legality of specific programs. In the event a certification is made but is challenged by the federal government as being untrue, Executive Order 14173 provides that the contractor may be subject to False Claims Act liability, which can result in a judgement of treble damages, civil penalties, loss of federal government contracts, and criminal penalties.

Changing DEI Disclosure Practices Across the S&P 500

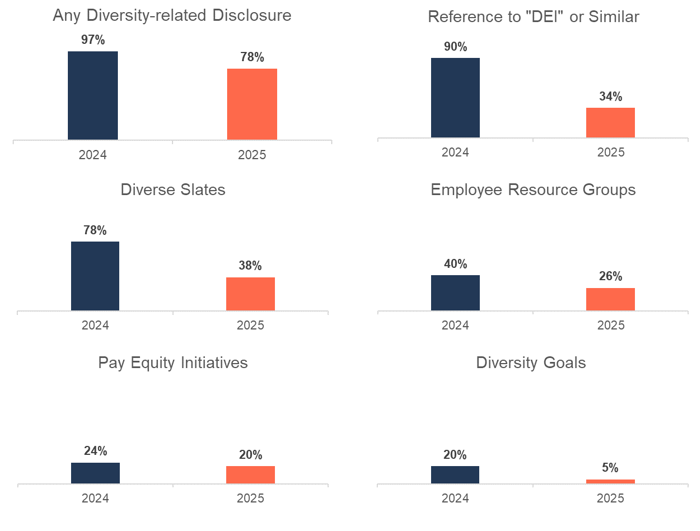

Since January 2025, 59 percent of the S&P 500 significantly revised or removed DEI-related disclosure previously made in the 10-K. Across the index, references to “DEI” or similar language fell significantly; only 34 percent of the S&P 500 used the term “DEI” or similar in their most recent 10-K, down from 90 percent in 2024.[3] However, while most companies no longer use “DEI”, 78 percent of the S&P 500 still had at least one diversity-related disclosure in their most recent annual report.

Specific diversity-related disclosures retained in the annual report varied from company to company. 40 percent of the S&P 500 significantly revised or shortened DEI-related content that was previously disclosed in 2024, rather than remove DEI-related disclosure outright. In many cases, companies replaced entire paragraphs previously dedicated to describing DEI-related programs and values with a shortened, diversity-related value statements such as a commitment to ‘deliver a positive workplace culture’. While the overall disclosure of DEI-related initiatives fell, many companies still disclosed at least one DEI-related initiative such as employee resource groups.

Only 19 percent of the S&P 500 that previously had DEI-related disclosure in the annual report entirely removed DEI-related content from their most recent filings.

Changing DEI Disclosures for the S&P 500 [4]

Spotlight: The Financial Sector

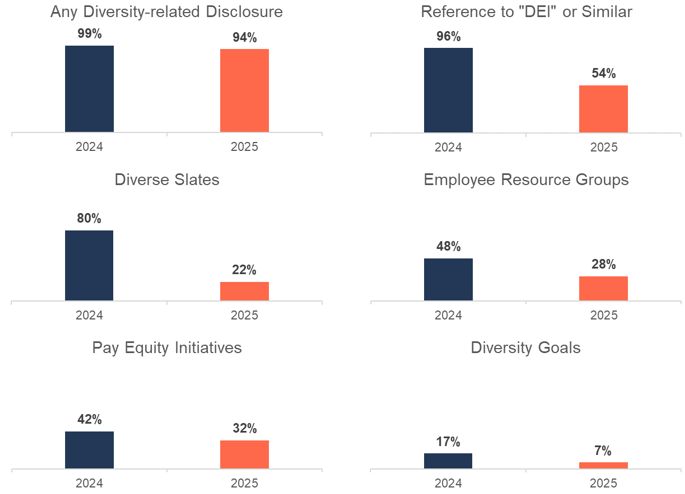

The approach to DEI-related disclosure varied across industries. As an example, we analyzed DEI-related disclosure for financial sector companies in S&P 500.[5]

A significantly greater proportion of companies in the financial sector revised DEI-related disclosures from 2024 to 2025, relative to the rest of the S&P 500. 74 percent of companies in the financial sector significantly revised DEI-related disclosure, compared to 40 percent of the entire S&P 500. Financial sector companies also shortened the length of DEI-related disclosure in the annual report to a greater extent. The average word count of DEI-related content fell by 42 percent for companies in the financial sector from 2024 to 2025, compared to 34 percent for the full S&P 500. While 19 percent of the S&P 500 entirely removed diversity-related disclosure from the annual report, only 4 percent of the financial sector did the same.

Changing DEI Disclosures for the Financial Sector [6]

Changing DEI Disclosure in the Proxy Statement

Reviewing recently filed proxy statements, we found that the trend to remove DEI-related disclosures from SEC filings is accelerating. More than 9 percent of the S&P 500 removed DEI-related content from the most recent proxy statement after not removing it from the most recent 10-K.[7]

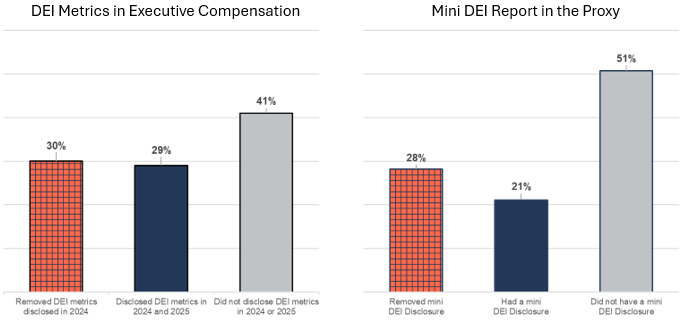

Looking at disclosure across the Fortune 100, we found a significant drop in DEI-related content from 2024 to 2025, including disclosure related to executive compensation and disclosure related to company DEI programs.

Disclosure of DEI-related metrics used for executive compensation programs across the Fortune 100 fell significantly from 2024 to 2025. In 2024, almost 60 percent of the Fortune 100 disclosed in the proxy statement that DEI-related metrics were used to determine executive compensation, including short- and long-term incentive awards and cash bonuses. In 2025, 30 percent of the Fortune 100 removed or replaced these DEI-related executive compensation metrics. Where DEI-related metrics were replaced, we generally found that companies were using other human capital metrics, such as an employee engagement score or employee safety metrics. However, replacement was not typical and differed by industry, with companies in the financial sector generally removing DEI-related modifiers outright.

We expect this trend to accelerate, given that descriptions of executive compensation in the proxy statement are backward-looking and describe compensation decisions for the previous fiscal year. For many companies in the Fortune 100, executive compensation metrics disclosed in the most recent proxy statement were finalized in early 2024, in advance of the changing disclosure practices seen in 2025.

Disclosure describing corporate DEI programs also significantly dropped in proxy statements filed across the Fortune 100. In 2024, approximately 49 percent of the Fortune 100 had a “mini DEI report” about their diversity-related initiatives in the proxy statement.[8] In 2025, only 21 percent of the Fortune 100 retained this disclosure, with 28 percent of the Fortune 100 removing this disclosure from the proxy statement entirely.

Compared to 2024, no company in the Fortune 100 added significant new proxy statement disclosure of DEI-related metrics in executive compensation or company-wide DEI programs.

Changing DEI Disclosure for the Fortune 100[9]

![]()

What Comes After “DEI”?

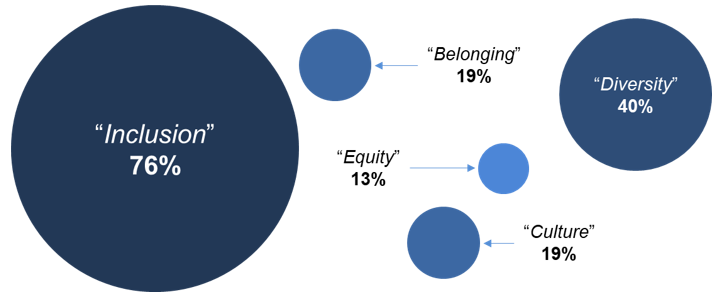

While many companies are retaining elements of DEI-related disclosure, only 34 percent of the S&P 500 used the term “DEI” to describe their diversity programs in 10-Ks filed since January. This is a major decrease from 90 percent in 2024. Instead, companies in the S&P 500 are replacing “DEI” with familiar language.

Where companies in the S&P 500 still have some DEI-related disclosure, 76 percent still used the word “inclusion”, 40 percent still used the word “diversity”, and 19 percent used “culture” or “belonging” to describe what was labeled as “DEI”. While “inclusion” is commonly used, and “diversity and inclusion” or similar is used by approximately 19 percent of relevant companies, there does not appear to be a clear consensus on a replacement term, although the trend to eliminate the word “diversity” will likely accelerate. Companies are taking different approaches to naming their programs, and we identified over 30 different phrases now used across the S&P 500 to describe these programs.

For example, we found the following phrases commonly used to describe diversity programs:

- Belonging and Culture;

- Equal Opportunity and Inclusive;

- Building a Diverse and Inclusive Workplace;

- Inclusion for All;

- Corporate Culture and Engagement;

- Inclusion, Diversity and Equal Employment; and

- Workplace Culture.

Revised DEI-related Program Names[10]

While many companies continue their commitment to diversity-related initiatives, the explicit use of the term DEI has notably declined. As companies navigate this evolving landscape and federal government enforcement of the Executive Orders that challenge DEI, companies are exploring new language and frameworks to communicate their commitment to fostering inclusive workplaces, reflecting a broader reevaluation of how DEI is or is not integrated into corporate identity and reporting.

1 Our review covered annual reports and proxy statements filed with the SEC since January 1, 2024. Using both a key word search and manual review, we identified DEI-related content in annual reports filed with the SEC between January 1 and April 11, 2025 by 411 companies in the S&P 500, and identified changes in DEI-related disclosure compared to the same filing from the previous year. Additionally, we reviewed proxy statements filed with the SEC between January 1 and May 9, 2025 by 71 companies in the Fortune 100 to identify changes to DEI-related disclosure. (go back)

2 Signed by President Lyndon Johnson in 1965, Executive Order 11246 laid out obligations for federal contractors to promote equal opportunities for women and minorities. (go back)

3 We used a key word search to identify the use of “DEI” or similar, searching for program names using different combinations of terms including “diversity”, “equity”, “inclusion” and “belonging” (go back)

4 Percentages based on the prevalence of relevant DEI disclosure in annual reports filed from January 1, 2025 to April 11, 2025 by 411 companies in the S&P 500 (go back)

5 Financial sector companies in the S&P 500 were identified based on the Global Industry Classification Standards (GICS). Financial sector companies included banks, insurance firms, investment companies, and other financial service providers. Using GICS codes, we identified 69 financial sector companies in the S&P 500 which had filed their 10-K between January 1 and April 11, 2025. (go back)

6 Percentages based on the prevalence of relevant DEI disclosure in annual reports filed from January 1, 2025 to April 11, 2025 by 411 companies in the S&P 500 (go back)

7 Based on a review of proxy statements filed from January 1, 2025 to May 1, 2025 by 416 companies in the S&P 500. (go back)

8 For our review, a company was considered to have a mini DEI report if they had disclosure at least two of the following from in proxy statement: a DEI values statement, workforce demographics, information on DEI goals, references to ERGs, discussion of DEI workstreams (including trainings or recruiting events) and supplier diversity initiatives.(go back)

9 Percentages based on disclosure from 71 companies in the Fortune 100 which filed a proxy statement between January 1, 2025 and May 9, 2025(go back)

10 Percentages based on disclosure from 411 companies in the S&P 500 which published an annual report between January 1, 2025 and April 11, 2025. (go back)

Distribution channels: Education

Legal Disclaimer:

EIN Presswire provides this news content "as is" without warranty of any kind. We do not accept any responsibility or liability for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

Submit your press release